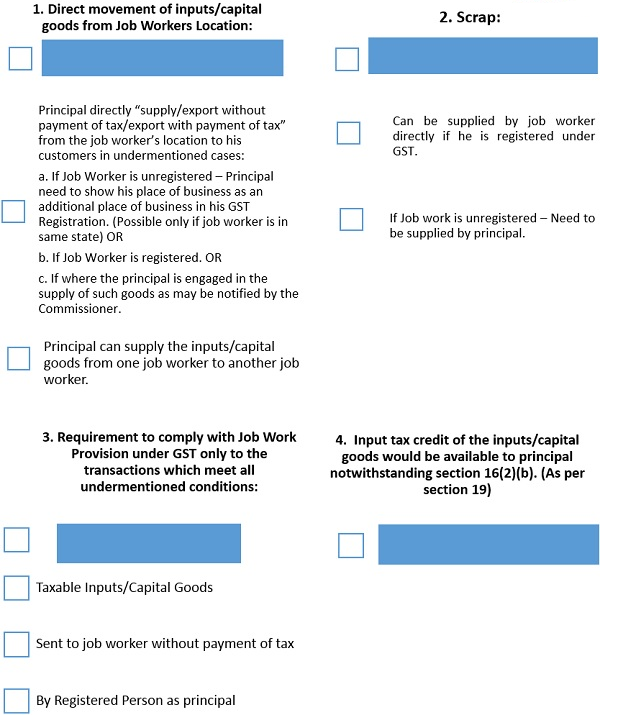

Job work means any treatment or process undertaken by a person on goods belonging to another registered person. So registered person need to send inputs/capital goods to job worker to do job work. To send these inputs/capital goods without payment of tax only on challan basis – Job Work provision under #GST comes into force.

Conditions to be fulfilled by principal to take benefits:

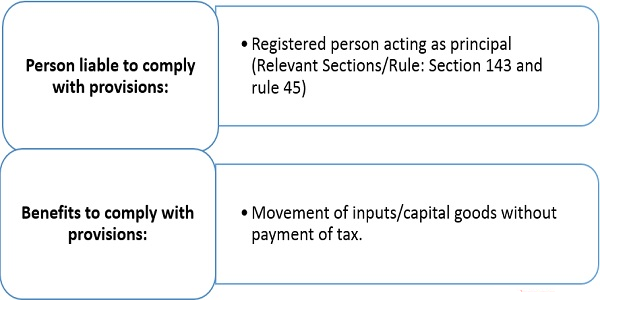

1. Need to maintain records as per section 143 & rule 45

- Movement of inputs/capital goods must be along with challans

- Proper record maintenance of inputs/capital goods sent, received back and pending for receipts.

- #Ewaybill generation in applicable cases:

- E-way Bill need to be generated if consignment value exceeding Rs. 50,000.

- E-way bill need to be generated if interstate movement of good irrespective of the value of consignment.

2. Furnish the required details on quarterly basis in ITC-04

3. Take back the inputs/capital goods within undermentioned time limit:

- Inputs – within one year (on sufficient cause being shown to commission, time limit may further extend to one year more)

- Capital goods other than moulds and dies, jigs and fixtures, or tools – within three years (on sufficient cause being shown to commission, time limit may be further extended to two more years)

- Moulds and dies, jigs and fixtures, or tools sent out to a job worker for job work– No time limits.

Consequences to be kept in mind if inputs/capital goods are not “received back/supplied/exported from job worker’s place” within prescribed time limit

1. Such Inputs/capital goods would be deemed to be supply and liable to tax from the under mentioned date:

- If inputs/capital goods supplied from the place of principal – Date of sending the inputs/capital goods.

- If inputs/capital goods sent directly by the supplier of principal to job worker’s location – Date of receipt of inputs/capital goods by job worker.

2. Supply need to be mentioned accordingly in the GSTR1

3. Need to pay the tax and interest on tax from date of deemed supply to the date of actual payment.

Some special points